The power to extract value from the value chain

Monopoly Power and the control of global supply chains

In this series of long reads, we examine the manifestation of monopoly power across various sectors and countries. We want to unravel the complex ties between corporate concentration and power, focusing on four key aspects:

- The power to extract profits.

- The power to distribute profits.

- The power to extract value from a value chain.

- The power to profit without producing

About the series

We researched these four dimensions using data from 51,000 publicly listed firms, over 100 countries, and 180 exchanges over the past three decades. We particularly emphasise the largest 1 per cent of publicly listed firms worldwide (by market capitalisation), providing fresh insights and discussing each dimension in detail.

In the first article, we looked at the power to extract profits. In the second article, we looked at the power to distribute profits away from innovation, employees and workers, and production to shareholders. Now, we focus on the vertical monopoly power of the top 1% of the biggest companies (by market capitalisation) and their power to extract value from the value chain.

Lead firms

Vertical monopoly power is built around lead firms that, according to the International Labour Organization (ILO), “control the global supply chain and set the parameters that other firms in the chain must meet, and are usually responsible for the final sale of the product.”

Since the 1990s, two aspects exacerbated vertical monopoly power. The first is the rise of intangible assets (patents, software, trademarks, and copyrights), which increased the power of the largest firms to profit without producing. The second aspect is the growing global economic integration by the rise of global value chains (GVCs).

These value chains provide leverage to lead firms through the control of intangible assets. Lead firms design products in one country, outsource the production of components in several other countries, and assemble the final product in yet another country (or countries).

Gatekeepers

The logistics, the standards, the terms of exchange and the overarching brand that operate as gatekeepers to end users can all be transformed into separate intangible resources by lead firms and monetised as rent-generating assets. This way lead firms control the financial reward for the different segments of capital employed in the different stages of production.

Apple

A well-known vertical monopolist is Apple. When it comes to electronics such as iPhones, iPads and computers, Apple controls the intangible assets at the start of the value chain (the technology, the design), and at the end (the brand, the copyright, the software licenses). The ownership of these essential intangible assets enables the firm to extract value from the intermediate steps in production, from raw materials, to intermediate goods, and assembly.

Drained supply chains

Vertical monopoly power results in large parts of the supply chain being drained of financial resources, while shareholders see their payout skyrocket and lead firms and intellectual monopolies increase their profit margins compared to other firms.

Our research shows that the biggest firms disproportionately increased the share of intangible assets, spend less on suppliers, and have higher payout ratios to their shareholders.

If we look at the 1 per cent of firms with the largest stocks of intangible assets, we see that they increased these from USD 1,612bn to USD 8,859bn in the period 2004 to 2023. In the same period, the group of firms constituting the bottom 50 per cent (based on their intangible assets), increased them from USD 13bn to USD 36bn.

This significant imbalance in ownership and control of intangible assets and the rentier income from leveraging these resources are the key markers of vertical monopoly power.

Skewed economic development

The rise of intangible assets and Global Value Chains together created a specific economic environment that enabled monopoly power to grow significantly in particular sectors. This skewed economic development is underpinned by an international legal and institutional structure that protects intangible assets through trade and investment agreements.

This type of vertical monopoly power expresses itself in different ways across sectors. Big Tech and Big Pharma clearly lead the pack when it comes to effectively monetising intangible assets. But other, less knowledge-intensive sectors have also witnessed the growth of lead firms that extract disproportionate amounts of profits from supplier firms.

Vertical monopoly power is important because Global Value Chains have become the key organisational structure of all intercorporate capital and trade flows in the current phase of globalisation. The World Bank estimates that 50 per cent of cross-border global trade(opens in new window) is organised within GVCs, primarily concentrated in Southeast Asia, Europe and the United States.

Read more

GVCs are highly specific to sectors. Not every GVC operates under the influence of a lead firm that directs the supply of consumer products. In the electronics sector, for example, GVCs often function as clusters where important suppliers may hold monopolistic positions, providing vital components to major consumer product manufacturers. Companies such as Nvidia exemplify this, supplying essential AI chips to tech giants like Alphabet, Amazon, and IBM.

Asymmetric power relations

Due to asymmetric power relations, the global corporate structure of command and control operates by spatially separating parts of production and assets in different countries.

The outsourcing of labour-intensive parts of production to low-cost economies with poor regulation was a crucial part of lowering the value that is captured by tangible assets such as property, plants, and equipment.

The decline in costs as a result of outsourcing parts of the GVC to low-cost economies meant that the price of final products could be lowered, the profit margin for lead firms increased, and a larger share of the value generated by the GVC was distributed to shareholders.

This story of lower consumer prices, rising profit margins for lead firms, and payouts to shareholders cannot be told without the integration of China into the global economy in the past 25 years. In this period, China became the workshop of the world, producing anything from electronics and apparel to automobiles.

The magic of this story is nothing more than the exploitation of the workforce and a lack of regulation in China and other low-cost economies combined with the growing legal protection of intangible assets by institutions dominated by the Global North. As the world of hyperglobalisation has stalled, the foundations of this source of wealth predation by vertical monopolists have become unclear.

How monopolies extract value

To understand the vertical monopoly power of the largest lead firms, it is essential to focus on the shift in the composition of capital stock. Historically, monopoly power has been associated with control over fixed capital, such as machines, factories, and other tangible assets.

During the past 20 years, there has been a substantial growth in intangible assets as a proportion of total assets. In the United States, for example, total assets of publicly listed companies grew by 341 per cent from 2004 to 2023, while intangible assets rose by 606 per cent. In China, during a period of significant economic growth, publicly listed firms saw total assets increase by 2,031 per cent, with intangible assets surging by 6,121 per cent.

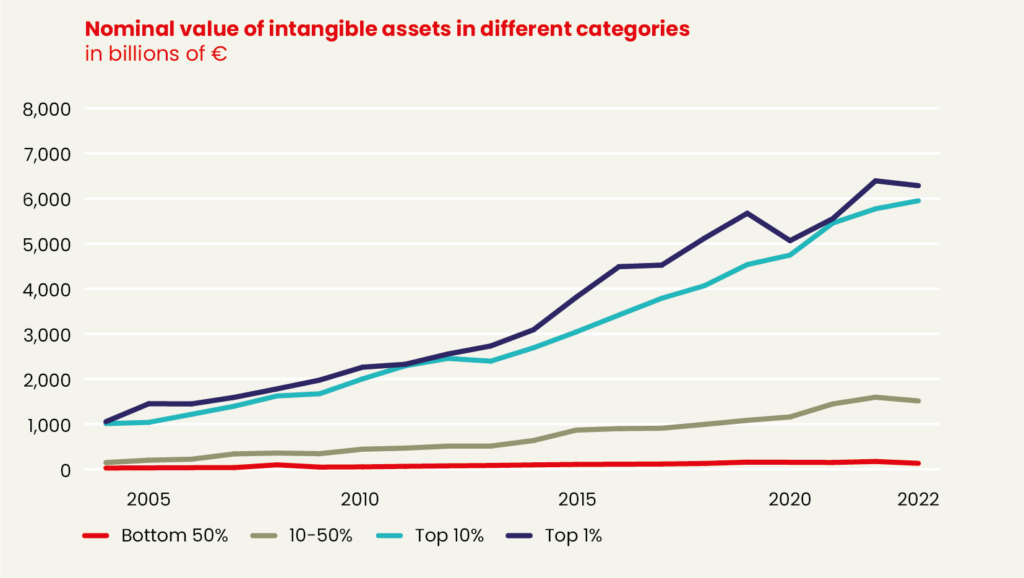

Comparing the largest 1 per cent of publicly listed global firms by market capitalisation, to the bottom 50 per cent, reveals a growing disparity in the value of intangible assets over the past 20 years.

In 2004, the largest firms had a total nominal value of intangible assets of EUR 1,056bn, which increased to EUR 6,286bn by 2023. In contrast, for the bottom 50 per cent, the value rose from EUR 27bn to EUR 131bn in the same period. As a result, the 370 most valuable firms (the top 1 per cent) in 2023 had 48 times more intangible assets on their balance sheets than the 19,638 firms in the bottom 50 per cent.

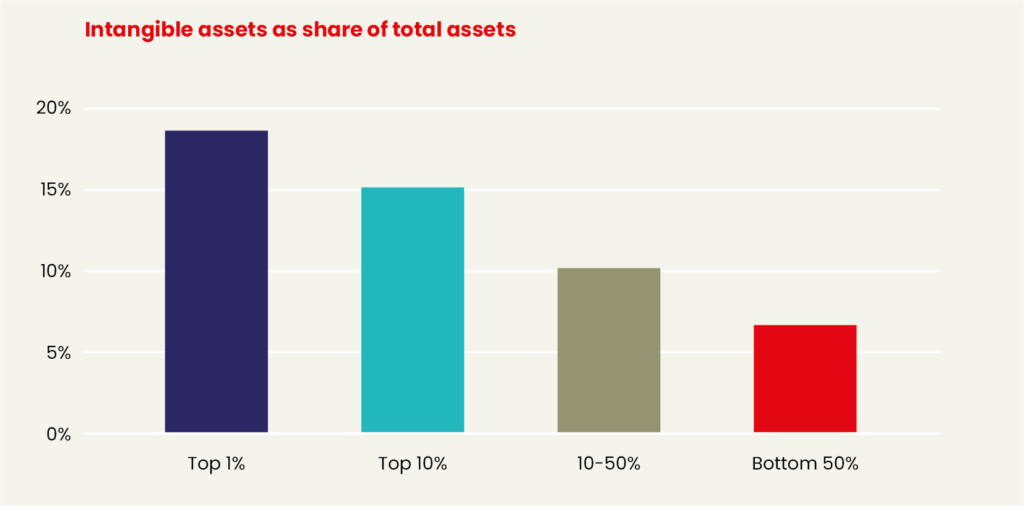

Intangible assets as a share of total assets are also unevenly distributed. Among the largest 1 per cent of firms, intangible assets constitute 18.7 per cent of total assets. For the bottom 50 per cent, this is 6.6 per cent.

More intangible assets allow firms to spend less on suppliers

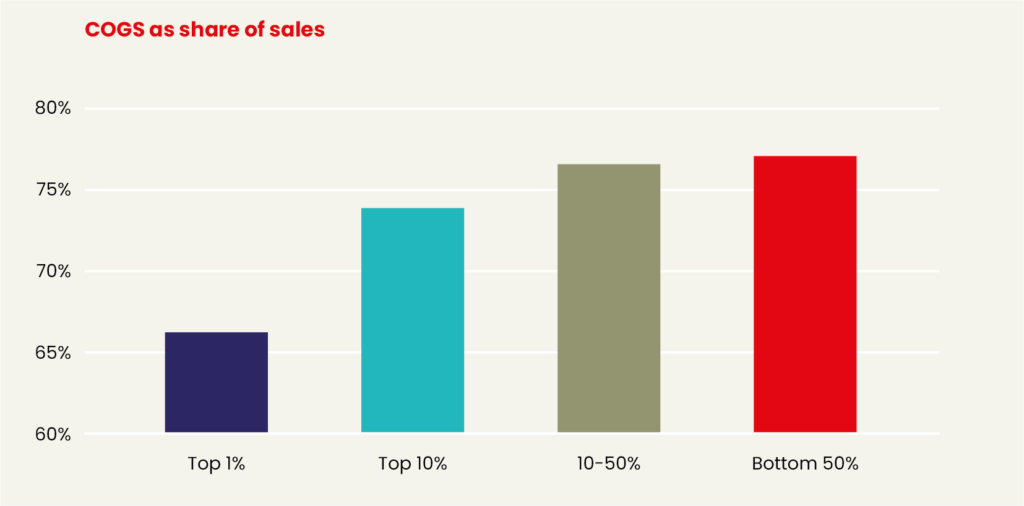

A second element we need to understand in vertical monopolies involves the share that these firms spend on suppliers, which we approximate by the accounting item ‘cost of goods sold’ (COGS).

COGS is also an indication for markups discussed in previous articles of this series. Essentially, low COGS relative to sales allow a firm to maintain a margin usable for various purposes. Conversely, spending a large portion of sales on COGS results in smaller markups and fewer financial resources for shareholder rewards, reinvestment, or R&D. In a competitive market, firms would see shrinking margins between sales and COGS.

Our analysis indicates that the largest (by market capitalisation) 1 per cent of firms have significantly lower COGS compared to the bottom 50 per cent. The 1 per cent have COGS constituting 66.2 per cent of sales, whereas the bottom 50 per cent have COGS at 77.1 per cent of sales.

If the top 1 per cent were to allocate the same share of sales to COGS as the bottom 50 per cent, they would spend an additional EUR 1,925bn on suppliers and wages in 2023, substantially reducing cash flows available to shareholders.

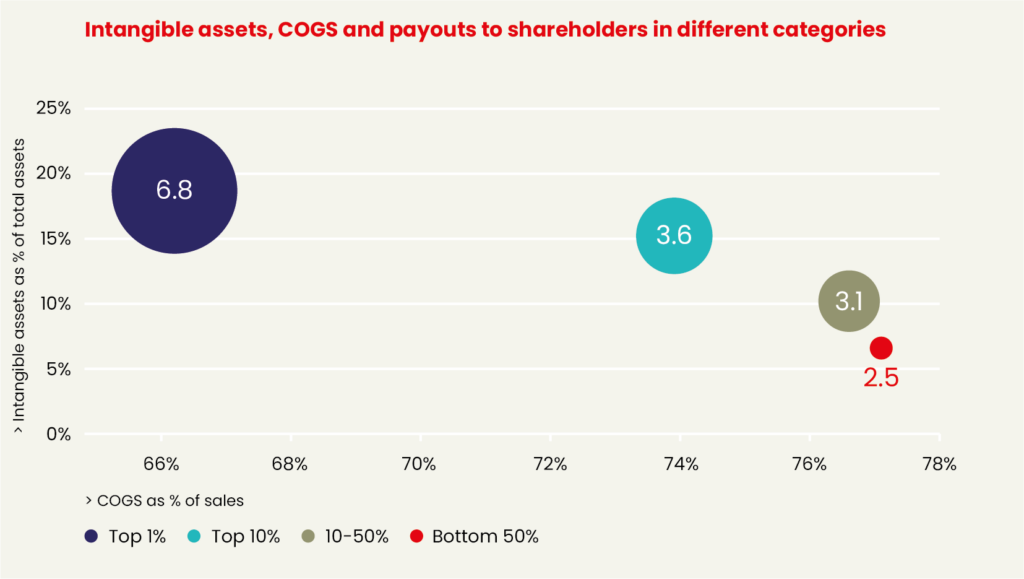

If we combine these different dimensions, we see the corporate power dynamics at play. Our analysis shows a relation between (1) firms having a large share of intangible assets to total assets, (2) having a low share of sales being spent on COGS, and (3) having larger payouts as a share of sales. In the table below we can see the three dimensions for the different clusters.

| Cluster | Intangible assets as share of total assets (in %) | COGS as share of sales (in %) | Payout to shareholders as share of sales (in %) |

|---|---|---|---|

| Top 1% | 18.7 | 66.2 | 6.8 |

| Top 1- 10 % | 15.2 | 73.9 | 3.6 |

| 10 % to 50 % | 10.2 | 76.6 | 3.1 |

| Bottom 50 % | 6.6 | 77.1 | 2.5 |

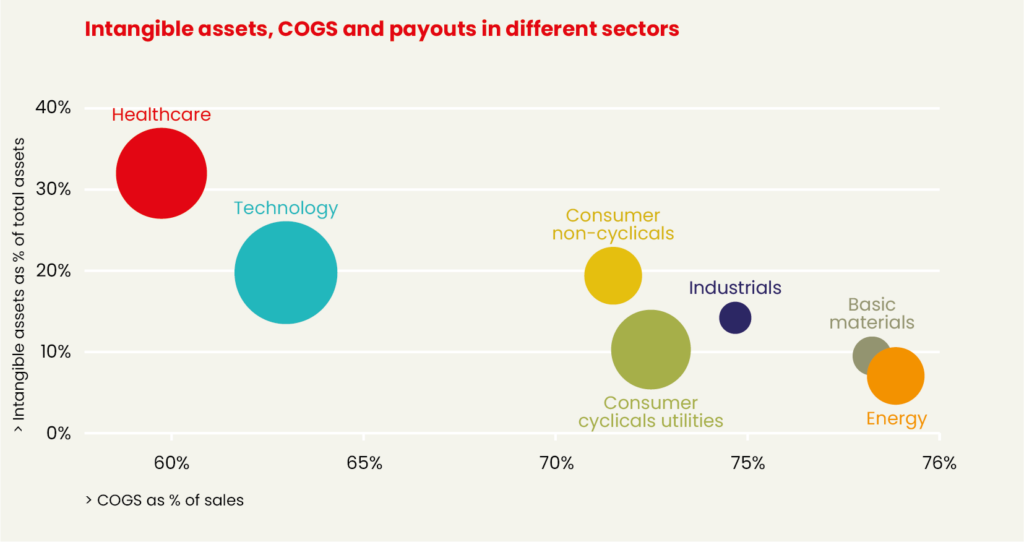

The figure below shows the size of intangible assets as a share of total assets on the horizontal axis, the size of payouts as a share of sales on the vertical axis, and the ratio of COGS to sales reflected in the size of the balloons. In the lower-left corner, we see the bottom 50 per cent of firms with a low ratio of intangible assets to total assets (6.6 per cent), combined with low payouts to shareholders (2.5 per cent) and a relatively large ratio of COGS to sales of 77.1 per cent.

There are significant sectoral differences in vertical monopoly power

Another way to look at the variety in vertical monopoly power of publicly listed firms worldwide is by focusing on separate sectors. The next figure shows separate sectors .

This figure portrays the average sectoral variations of the type of vertical monopoly power of our analysis and shows that in the health sector, primarily driven by underlying industries such as pharmaceuticals and biotech firms, we find the highest average combination of higher ratios of intangible, lower COGS, and high payouts to shareholders.

In the energy sector, shown on the opposite side of the figure, some industries have extremely high COGS ratios in downstream activities, such as petroleum refineries with COGS ratios of 92 per cent. Conversely, some industries have very low COGS, such as in upstream activities like oil production and exploration, with COGS of 38 per cent.

A closer look at the apparel industry

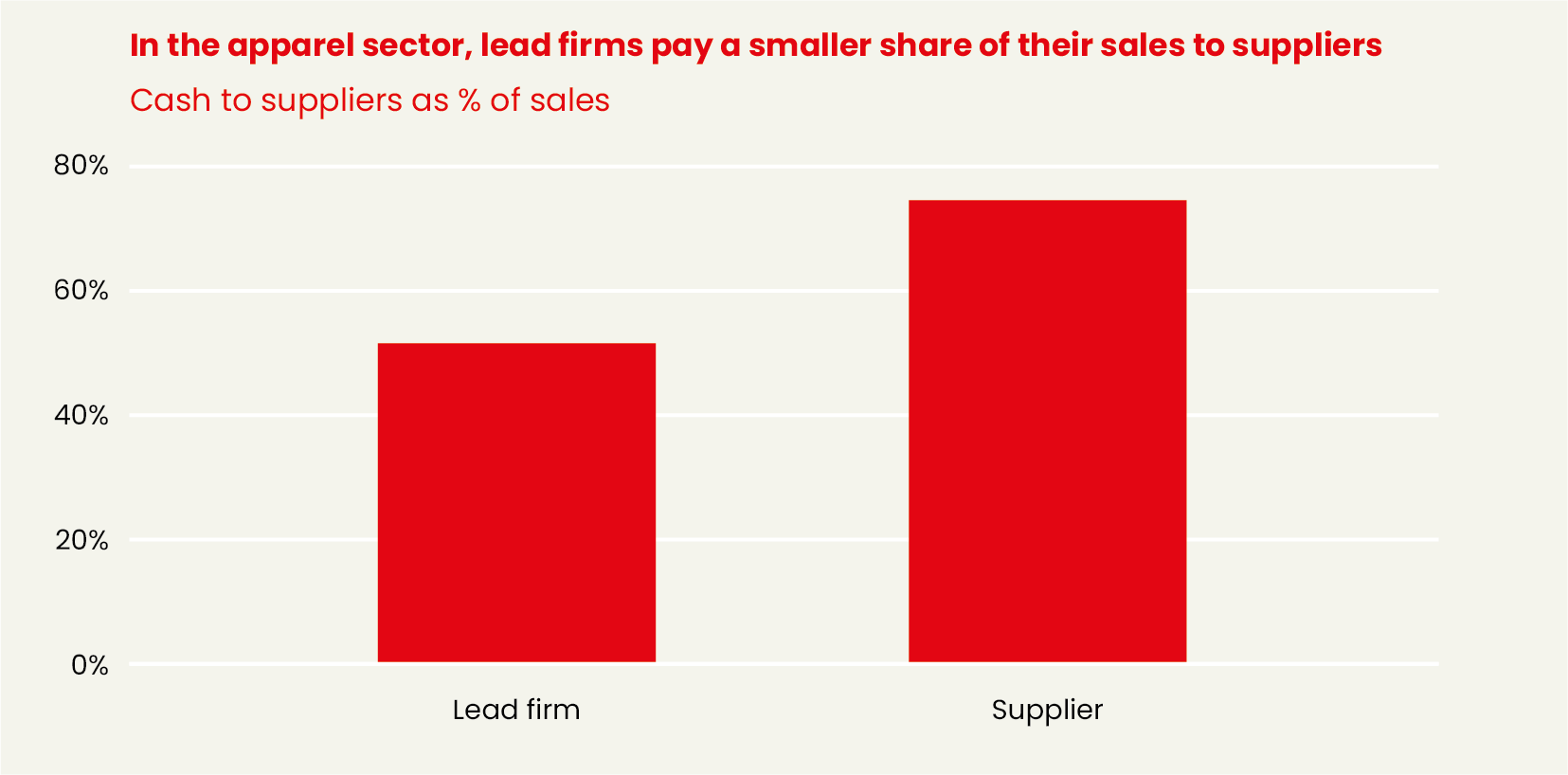

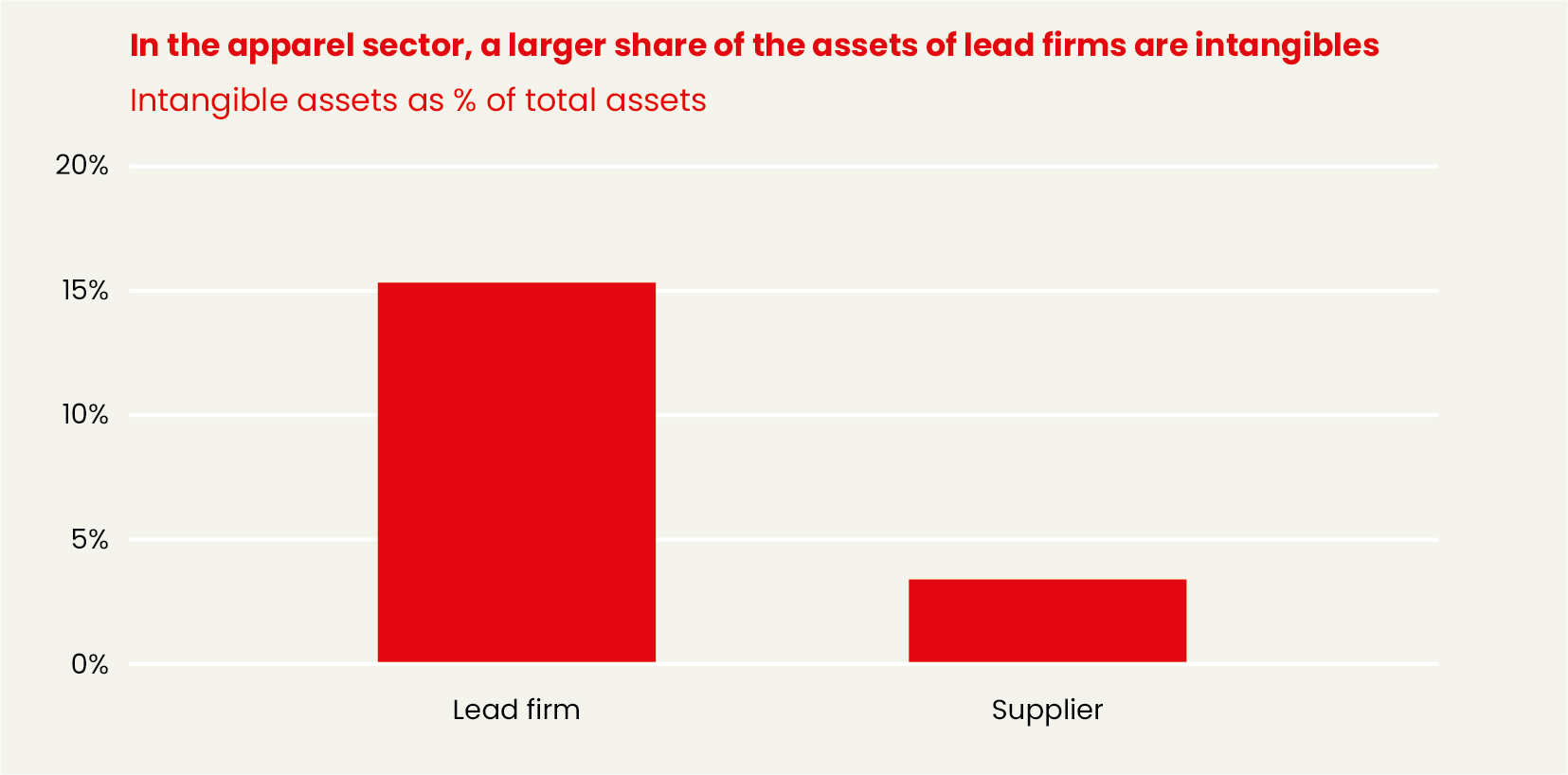

A closer look at the apparel industry uncovers crucial differences between lead firms and suppliers in the global value chain. These supplier firms, contract manufacturers, unlike typical smaller suppliers, are notable for being publicly listed and wielding considerable influence within the industry’s broader value chain.

By 2023, these suppliers had amassed total assets valued at EUR 85.4bn, which is markedly less than the EUR 319.6bn held by the lead firms in that same year. These supplier entities find themselves sandwiched between minor, less influential suppliers and the well-resourced lead firms that serve as gatekeepers to the industry.

If we compare these two groups of firms, we clearly recognize a difference in the three ratios we have been looking at (1) the COGS to sales, (2) the intangible assets to total assets, and (3) payouts to sales. The supplier firms portrayed here have significantly lower Intangible assets, spend a larger part of their sales to suppliers, and have lower payouts to their shareholders.

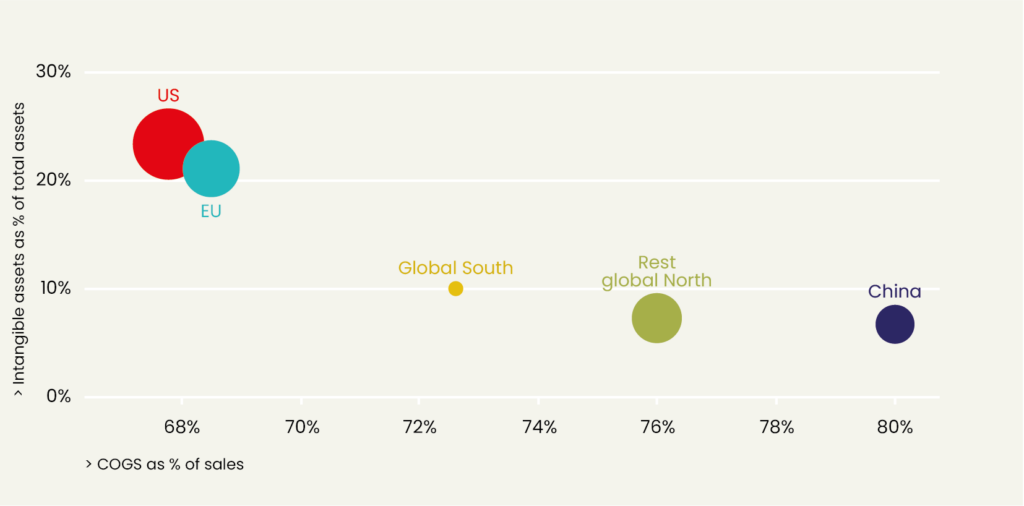

The group of lead firms is overwhelmingly composed of companies from the Global North, primarily in Europe, the United States, and Canada, with Zhejiang Semir Garment Co. from China being the sole exception.

These lead firms exhibit a wide range of financial ratios, highlighting diverse business strategies. For example, Prada in Italy boasts a notably low COGS to-sales ratio (22.5 per cent), whereas companies like Gap (63.6 per cent) in the United States and Gildan Activewear (74.3 per cent) in Canada have significantly higher ratios.

In contrast, the top 50 supplier firms are largely based in Japan, China, Hong Kong, Korea, Indonesia, and Vietnam, with most reporting COGS ratios above 70 per cent to 80 per cent. However, exceptions such as Bosideng International Holdings from Hong Kong (41.4 per cent) and Japan’s Wacoal Holdings (44.5 per cent) manage to operate both as lead and supplier firms, reflecting a dual operational capability.

These observations highlight a distinct geographical pattern, with lead firms dominantly emerging from the Global North, controlling most of the intangible assets, while supplier firms largely operate from the Global South, including China, Korea, and Japan, indicating a regional specialisation in roles within the global value chain.

Within this regional specialisation, the command over a massive labour force is outsourced to contract manufacturers (suppliers). These firms operate large, highly gendered workforces, often employing thousands of workers. They incorporate the labour-intensive tasks that brands (lead firms) outsource. To minimize labour costs, they cluster in low-wage countries, primarily in Southeast Asia, with vast ‘reserve armies’ of potential labour power.

Geography and the dynamics of vertical monopoly power

The emergence of vertical monopoly power, which enhances financial returns for those controlling intangible assets at the expense of those managing tangible assets, is intricately linked to the 1980s trend of outsourcing production from developed economies to developing regions. This shift was facilitated by a network of bilateral tax and investment agreements and the establishment of the World Trade Organization (WTO), most notably its TRIPS agreement dealing with intellectual property. This institutional architecture evolved just in time for China to enter the global economic integration framework by joining the WTO in 2001.

By classifying firms into national and regional categories, significant differences in financial ratios become evident. Companies based in the United States generally showcase high levels of intangible assets, low COGS, and high payout ratios, contrasting with the typical traits of Chinese supplier firms. Despite this, there has been a noticeable rise in powerful lead firms within China, signalling a shift in the economic landscape.

The giant Chinese corporations (in terms of sales and assets), part of the global 1 per cent, are most pronounced in technology , communications , energy , construction , railways and electric vehicles .

These large firms have become relatively detached from foreign-controlled GVCs and have grown significantly within the rising Chinese economy. Some of these firms have outgrown their domestic market and have started to export as lead firms. Chinese firms have moved to the forefront of key industries and technologies, outcompeting firms from the Global North. We see this in strategic sectors such as solar energy, wind turbines, and batteries; all crucial for the energy transition.

Most of the largest Chinese firms are state-owned enterprises(opens in new window) that can be considered part of an emerging regime of new state capitalism(opens in new window) that extends beyond China. The reorientation from foreign-controlled GVCs to the domestic economy is therefore part of a broader realignment wherein these state-owned enterprises are critical stepping stones in a state-led development strategy.

The new state capitalism in China and other emerging economies is also a key marker of the shift in the centre of gravity(opens in new window) of the global economy from the North Atlantic to the Pacific Rim. This is not only a geoeconomic transformation but also affects the mechanics of the rent-extracting business model built around vertical monopolies.

Growing hegemonic rivalries and the future of vertical monopoly power

The central role of China in carrying the heavy load for lead firms located in the Global North, and enabling them to leverage their control over intangible assets, may change as the global landscape starts to shift.

While the key turning point was the global crisis in 2008, the Russian invasion of Ukraine and the establishment of BRICS have resulted in disrupting the world of hyperglobalisation that dominated the global economy from the 1980s onwards.

Consequently, we have seen growing geoeconomic rivalries, leading to the adoption of increased protectionist measures and national industrial policies by different economic blocs, centred on strategic sectors such as semiconductors.

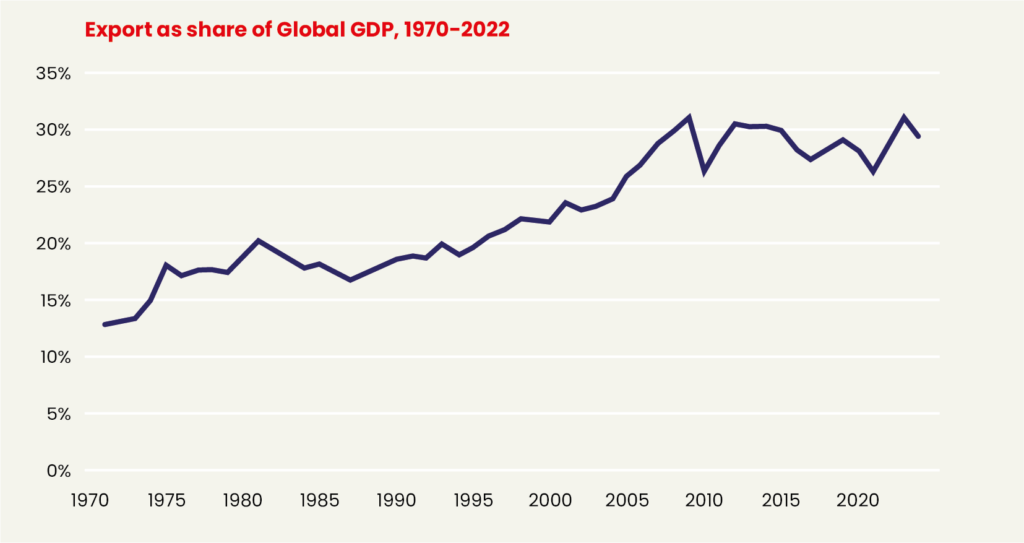

After a period of increasing GVC structures on the back of growing cross-border economic and financial integration, we have seen a slowdown of trade as a share of global GDP(opens in new window) since the financial crisis (see figures below).

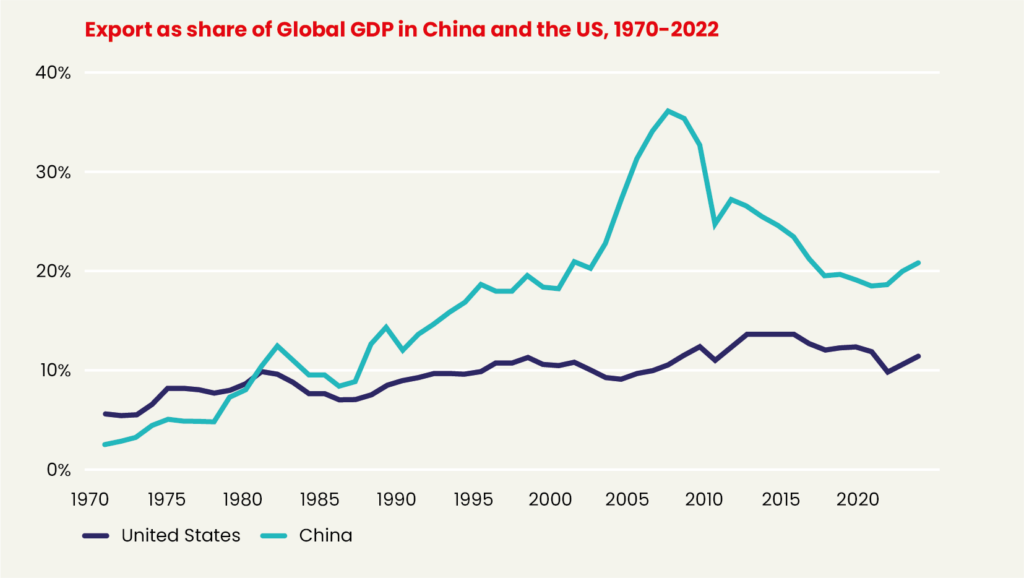

Trade as a share of global GDP increased from 12,8 per cent in 1970 to 18,9 per cent in 1990, and 30,9 per cent in 2008. Since then, trade as a share of GDP has hovered around this ratio declining to 29,3 per cent in 2023. China experienced a dramatic rise in exports (and imports) as a share of GDP after it joined the WTO (see figure on China below). But this growing share of exports reached a peak and declined rapidly after 2008, pushing down global export figures. Compared to the United States, China remains more reliant on exports.

As hegemonic contestation between the United States and China deepens, we may start to see a growing fragmentation(opens in new window) of GVCs. On the other hand(opens in new window) , the large interdependencies that have come to dominate the global economy, precisely because of the centrality of cross-border GVC, may also diffuse tensions as costs of fragmentation (too interconnected to fail) have become too big. The interdependencies go both ways; China is both the key exporter and importer of goods and services globally.

Whichever way developments go, it is clear that the structural elements that gave rise to GVCs since the 1980s and enabled firms from the Global North to dominate the allocation of financial flows, investments, and profits will cease to exist in the same form in the future.

The period of US-centred hyperglobalisation, underpinned by an uncontested neoliberal institutional framework, pushed forward by institutions that operated in the interest of the Global North, such as the IMF, the World Bank, and the WTO, will not return. This time there is a real alternative, which is growing in scope. This alternative is centred on China and other members of BRICS.

The exclusive rights firms from the Global North had over vertical monopolies, and the power to extract disproportionate value from GVCs by leveraging intangible assets may come to an end. This can feed into the unfolding polycrisis and interact with the growing electoral support for radical right, illiberal, nationalist political agendas that look inwards across the Global North and beyond.

This will increase insecurities over access to raw materials, technology, and intermediate goods, as competing economic blocks try to reposition their strategic influence. It is against this background that we may see vertical monopoly power feed into imperial contestation, as interdependencies between the state and the largest and most powerful firms surface, just as they did in the previous age of monopoly capitalism, heralding a new age of imperialism that culminated in WWI.

A way forward

To counter this darkest possible scenario, we need to diffuse hegemonic rivalry and develop political, diplomatic, and ideological pathways(opens in new window) for collaboration and peaceful coexistence between different economic blocks. The rise of China and the elevation out of poverty of hundreds of millions of people should be a cause for celebration.

There needs to be a radical makeover(opens in new window) of global financial and economic institutions, from the IMF to the WTO. Not only in terms of decision-making but also in outcomes. There should come an end to the perpetual debt crises in the Global South that shrink the fiscal space that is required for these countries to operate as sovereign democratic countries. The deeply entrenched structure of dependency that perpetuates underdevelopment, cannot be dismantled without pulling down the structures that enable vertical monopoly power to foster.

The excessive rentier income that vertical monopolies have enjoined over the past decades, will have to be redistributed fairly across value chains. This requires confronting corporate power and the excessive legal protection of intangible assets(opens in new window) that generate rentier income. Technology and the skills to access and use will also have to be distributed fairly(opens in new window) and regulated to allow for the rebalancing of value chains.

The prioritisation of shareholders discussed in the previous article on monopoly power, will also need to end. If priority lies in a just transition, this will need to be reflected in the value chains that connect different parts of the world.

Do you need more information?

-

Rodrigo Fernandez

Senior researcher

Related news

-

-

Taking Stock: 50 Years of prioritising shareholdersPosted in category:Long read

Rodrigo FernandezPublished on:

Taking Stock: 50 Years of prioritising shareholdersPosted in category:Long read

Rodrigo FernandezPublished on: -

Digital Markets Act: Big Tech’s pushback faces up to a bold EUPosted in category:Long read

Digital Markets Act: Big Tech’s pushback faces up to a bold EUPosted in category:Long read Margarida SilvaPublished on:

Margarida SilvaPublished on: